1.1 STATUS OF THIS DOCUMENT

This is the FpML 5.2 Reccomendation #2 for review by the public and by FpML members and working groups.

The FpML Working Groups encourage reviewing organizations to provide feedback as early as possible. Comments on this document should be sent by filling in the form at the following link: http://www.fpml.org/issues. An archive of the comments is available at http://www.fpml.org/issues/

There are also asset class-specific mailing lists; you can join them at the following link:

A list of current FpML Recommendations and other technical documents can be found at

This document has been produced as part of the FpML 5.2 activity and is part of the Standards Approval Process.

The FpML documentation is organized into a number of subsections.

This section provides an overview of the specification.

These are automatically generated reference documents detailing the contents of the various sections in the FpML schema.

- Core Definitions:

- Products:

- IRD

- FX

- CD

- EQD

- Bond Options

- Options shared

- Commodity

- Business Processes

- Reference:

- Index and cross-reference of definitions

- Schema and Example files - Provides zip file with FpML schemas and examples.

- Examples - Provides sample FpML for each section.

- Scheme Definitions - Describes standard FpML schemes, and the values that they can take.

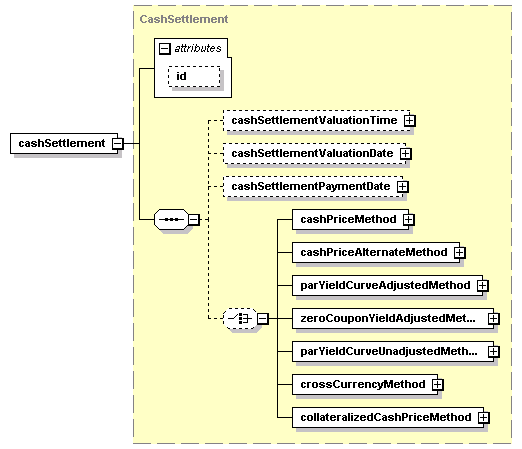

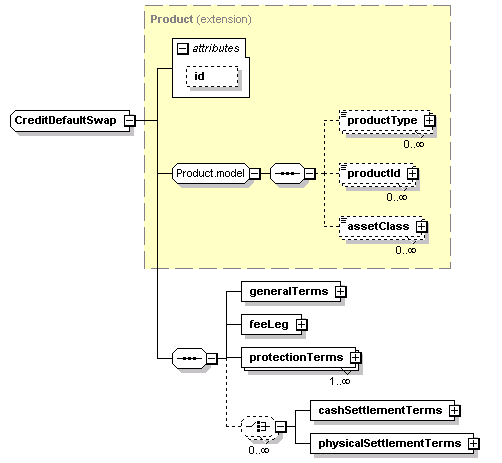

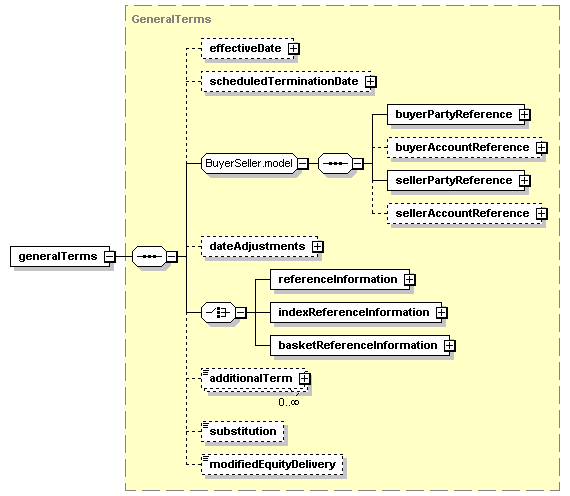

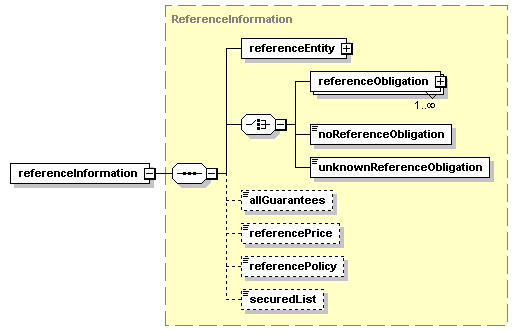

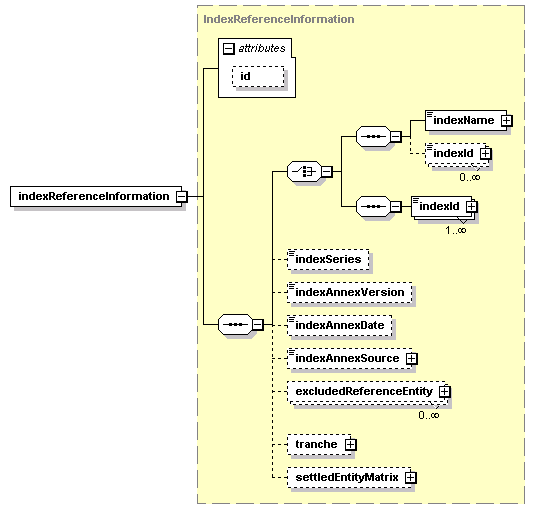

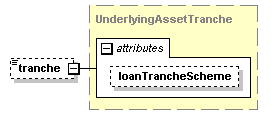

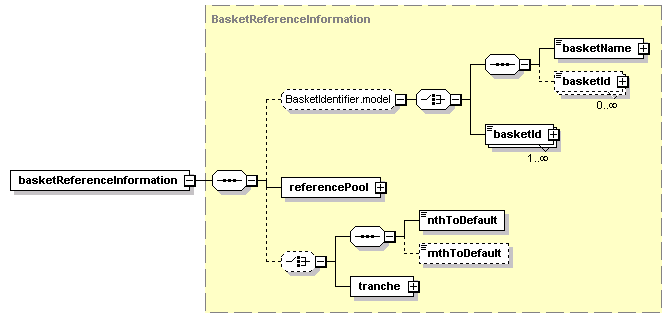

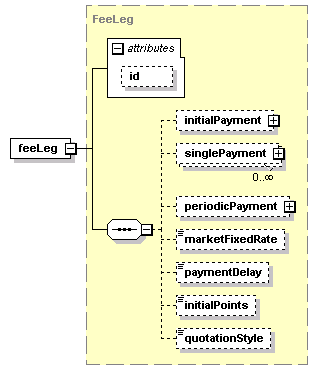

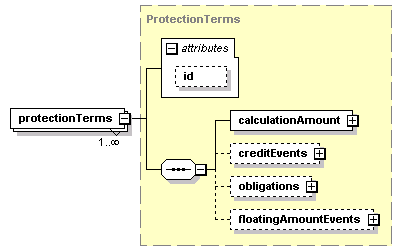

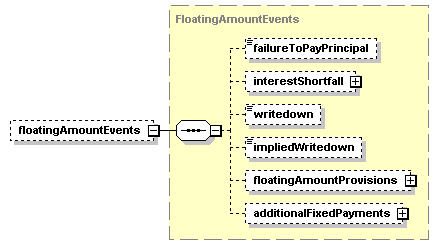

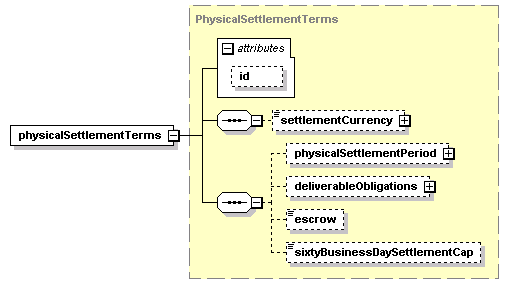

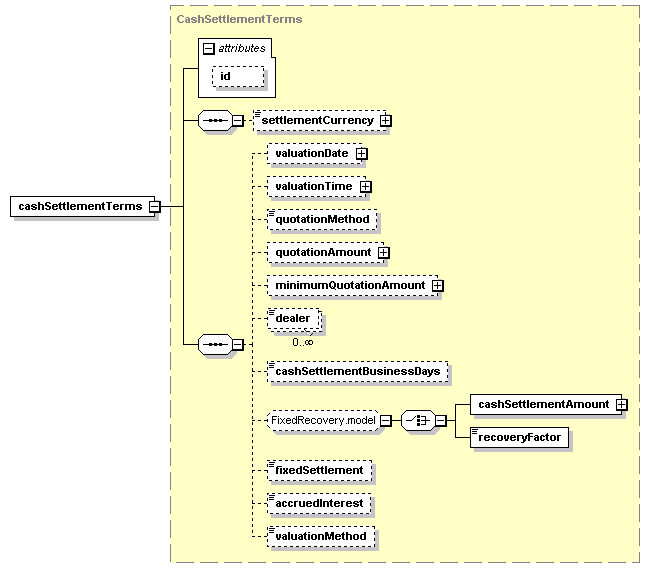

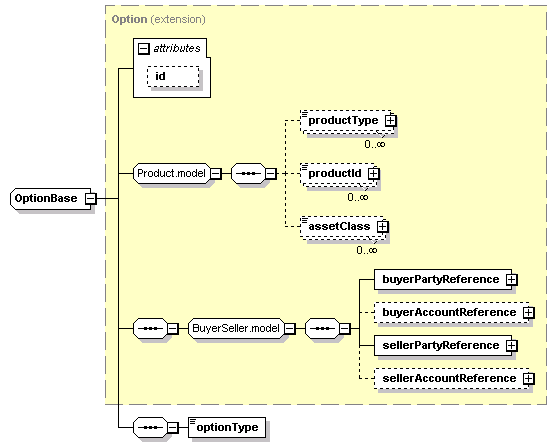

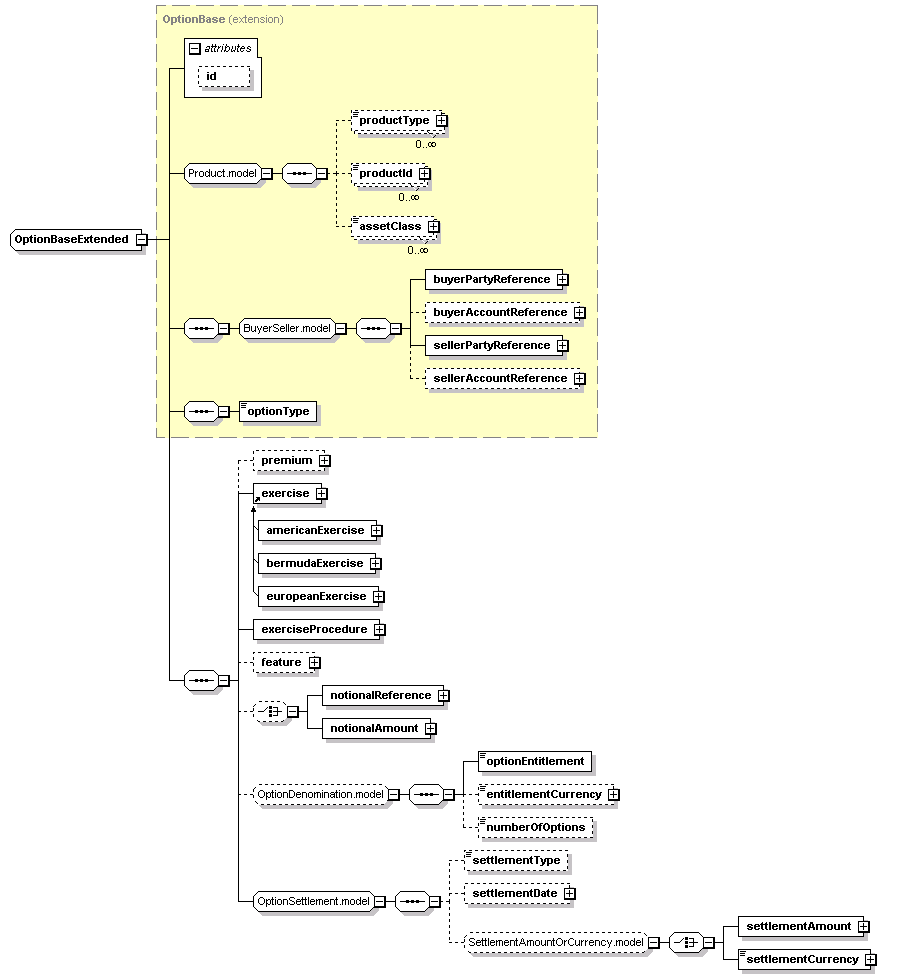

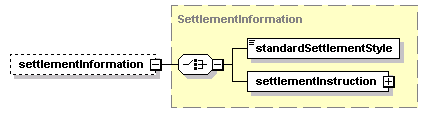

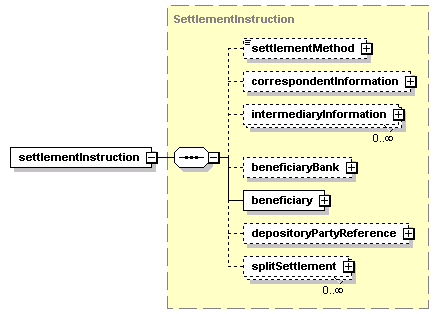

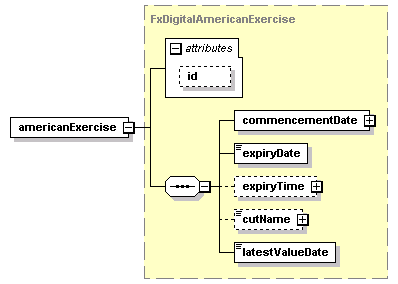

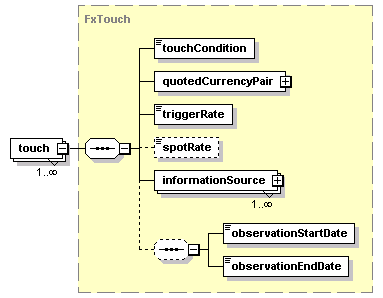

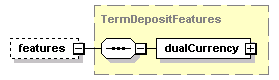

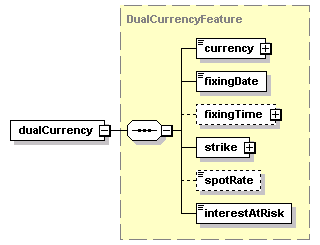

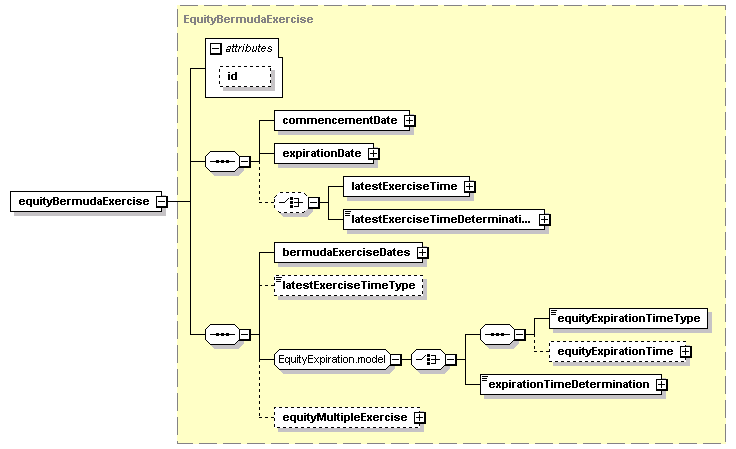

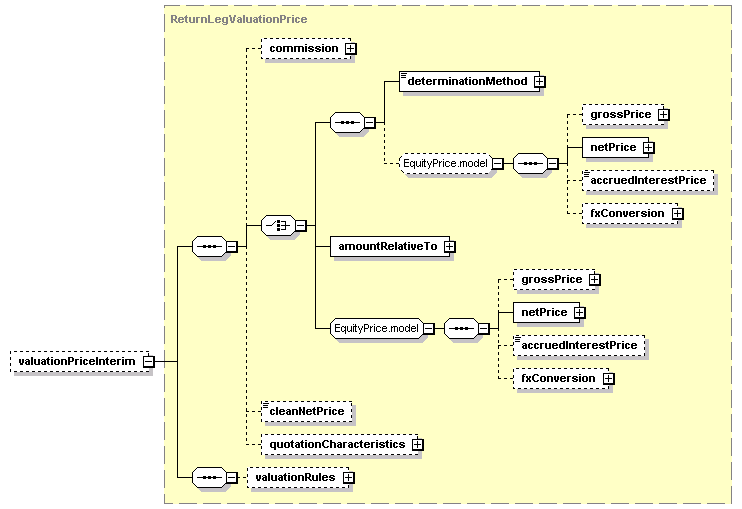

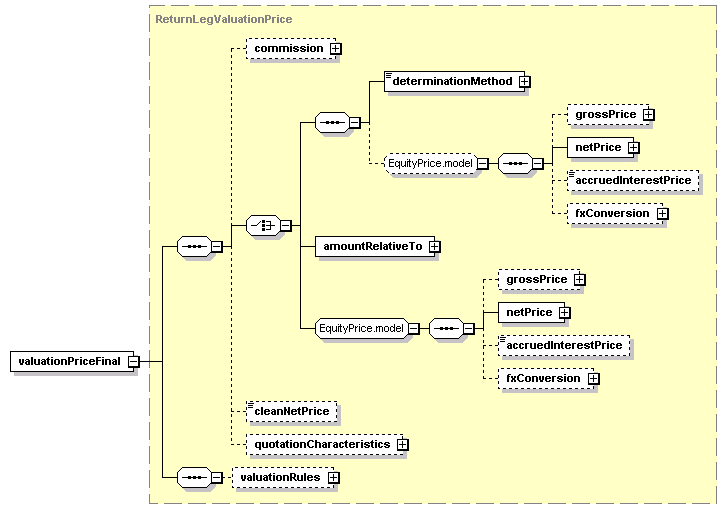

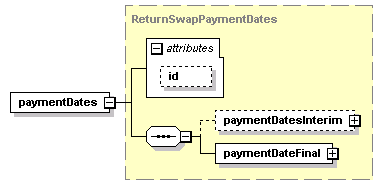

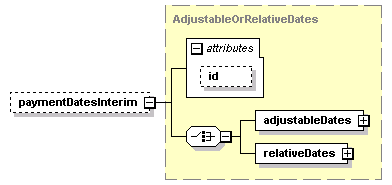

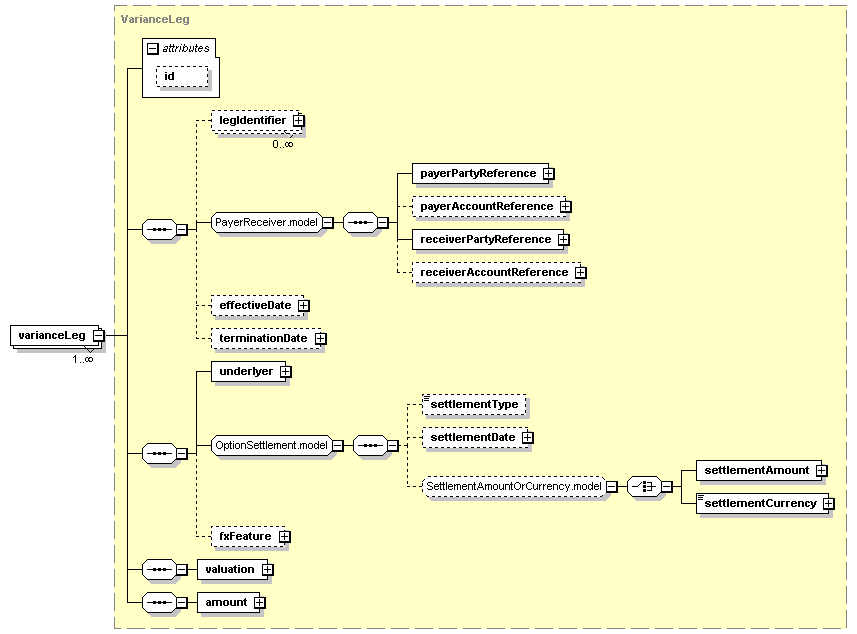

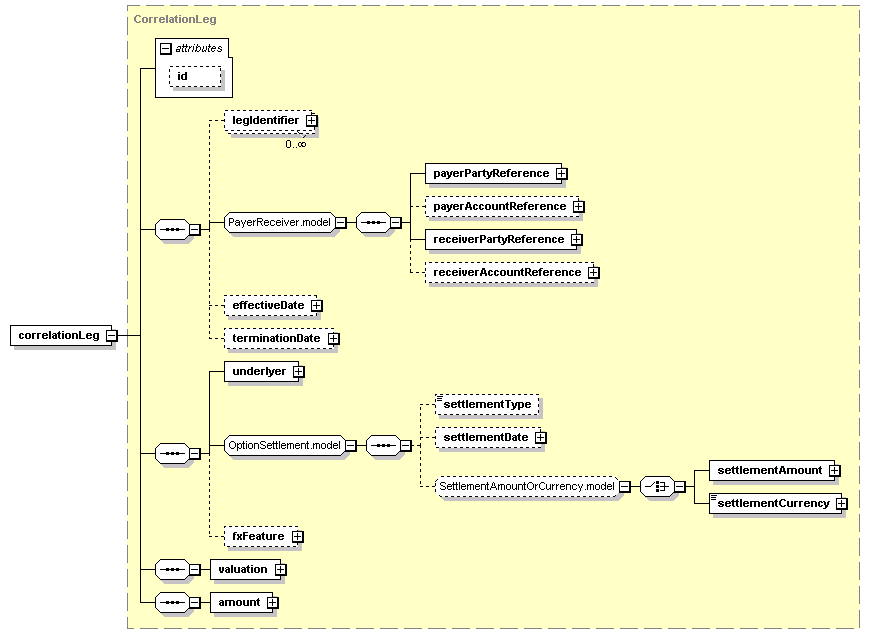

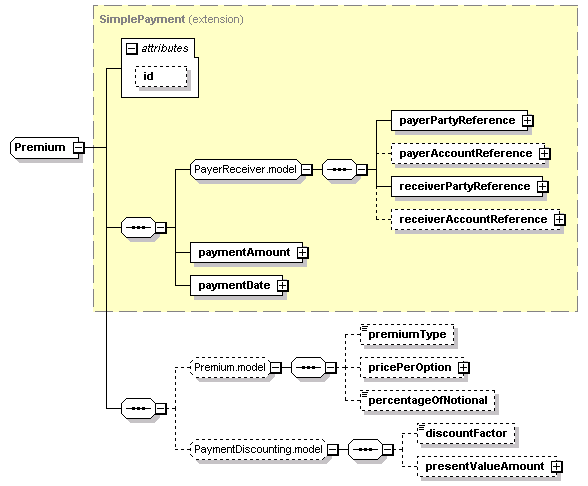

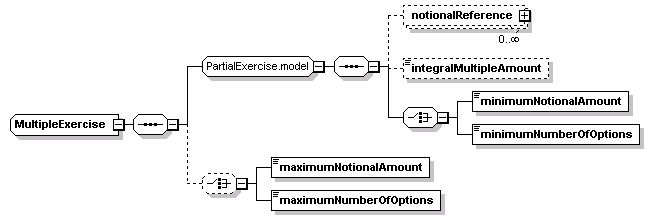

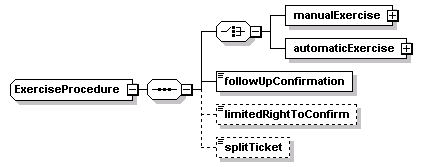

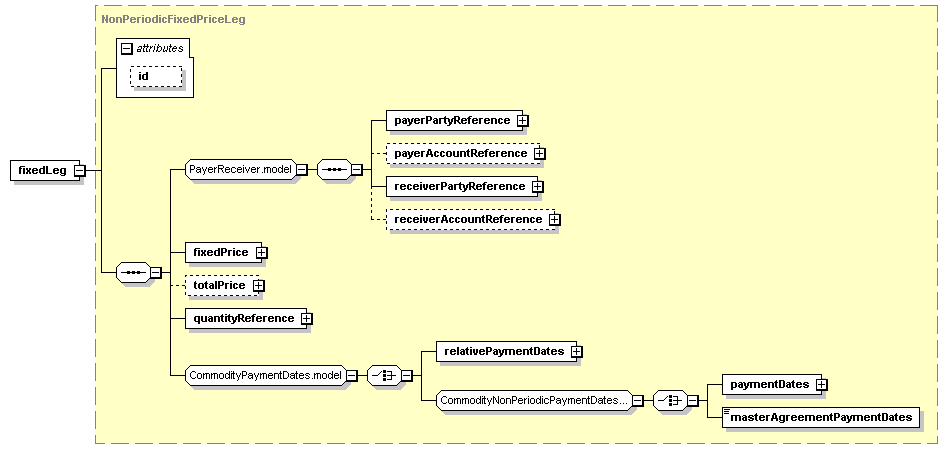

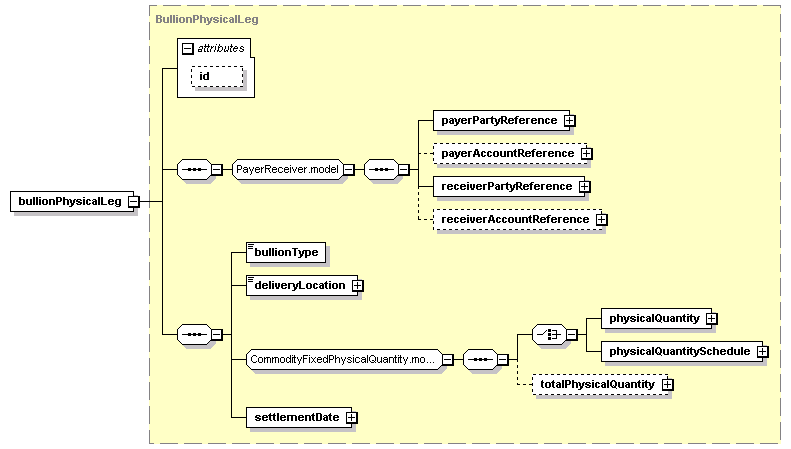

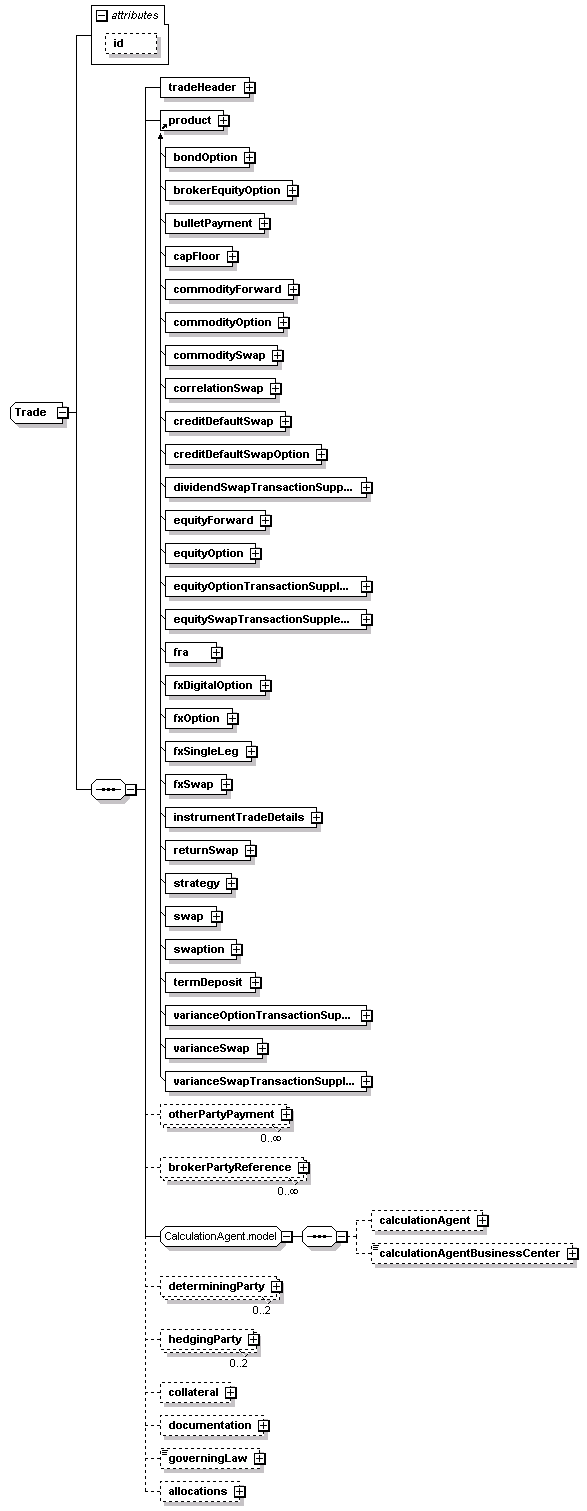

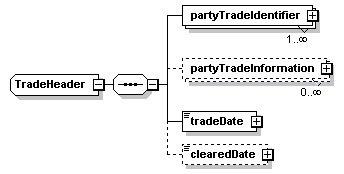

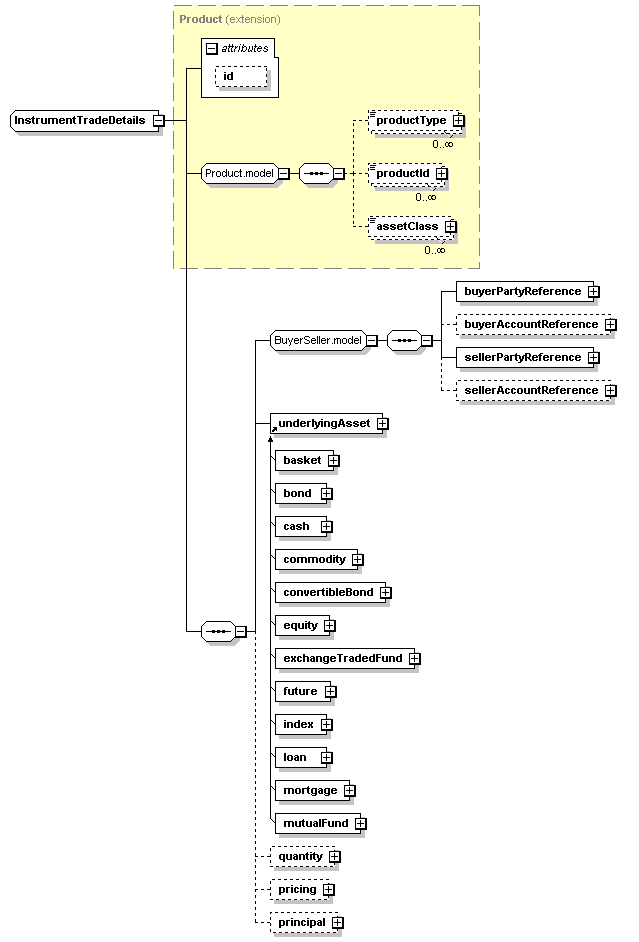

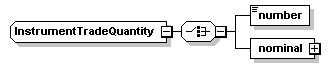

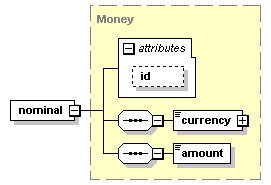

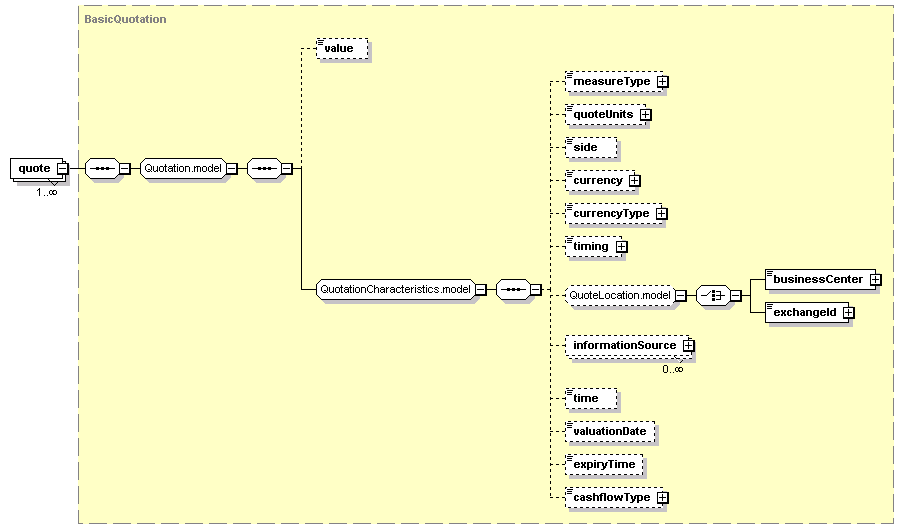

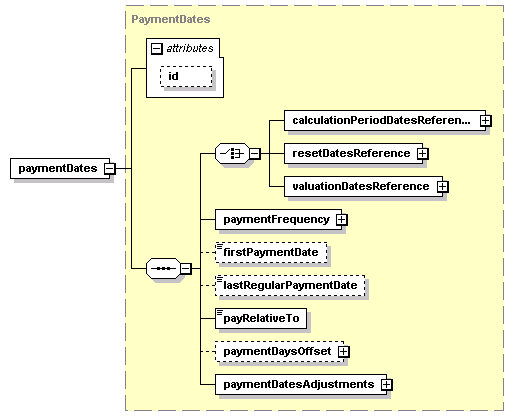

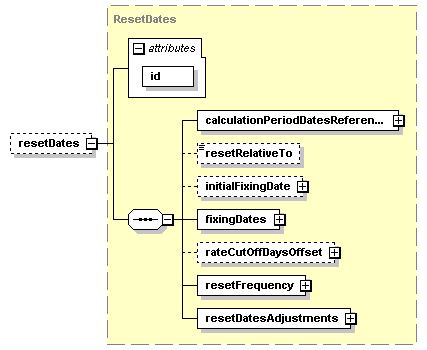

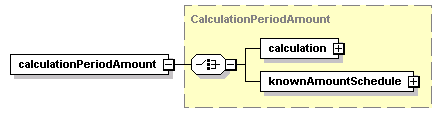

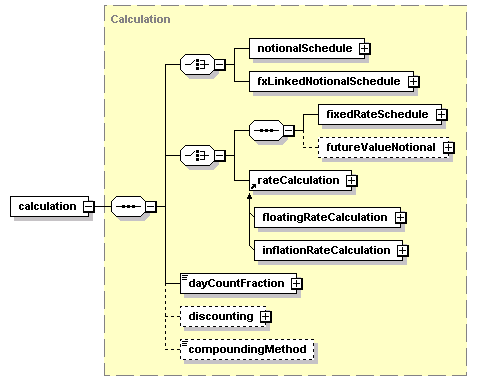

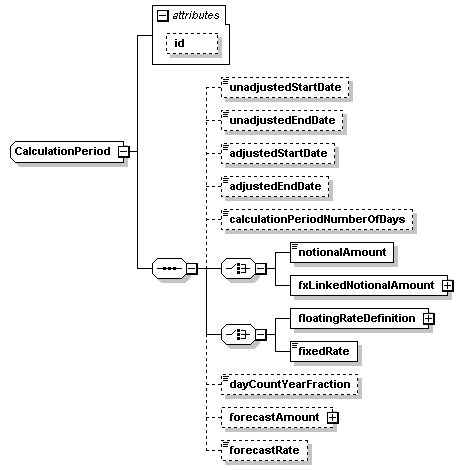

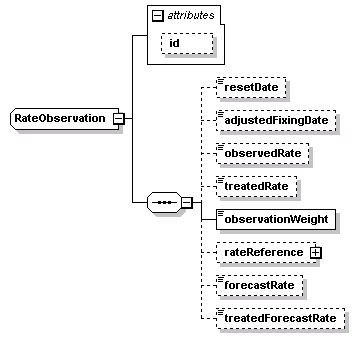

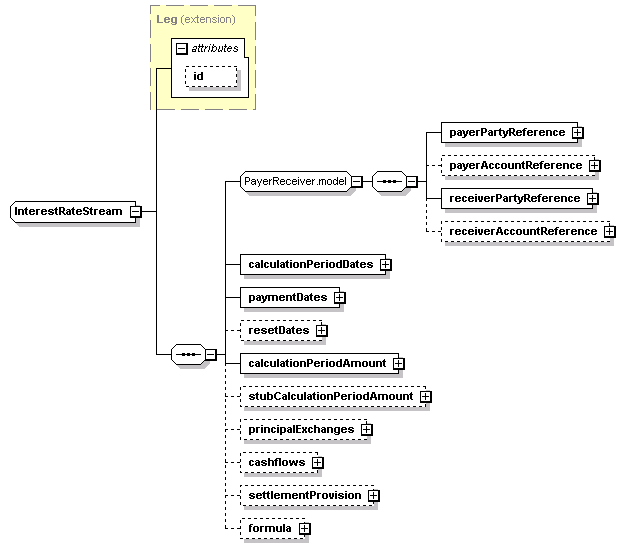

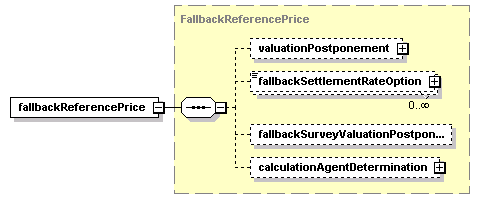

Most diagrams in this specification come from TIBCO's XML Turbo application which is used to batch generate the pictures in the documentation. The notation follows the pattern:

- No bubble indicates a mandatory element or attribute

- A '?' indicates an optional element or attribute

- A '*' indicates an occurrence of zero or many

- A '+' indicates an occurrence of one or many

- A '..' bubble with numbers above and below indicates specific range

- A '1' in a bubble indicates the presence of a nested sequence or choice group

- Diagonal lines indicate a choice group (< shape)

- Non-diagonal lines indicate a sequence ([ shape)

- A 'D' in a bubble indicates an attribute with a default value

This document was produced by the following working groups:

- Andrew Jacobs (HandCoded Software), chair

- Anthony B. Coates (Miley Watts)

- Igor Dayen (Object Centric Solutions)

- Daniel Dui (University College London)

- Marc Gratacos (ISDA)

- Simon Heinrich (IONA Technologies)

- Lyteck Lynhiavu (ISDA)

- Andrew Parry (JP Morgan Chase Bank)

- Raj Patel (HSBC)

- Henri Pegeron (MarkitSERV)

- Matthew Rawlings (JP Morgan Chase Bank)

- John Weir (Goldman Sachs)

- Irina Yermakova (ISDA)

- Brian Lynn (Global Electronic Markets), chair

- Andrew Jacobs (UBS)

- Andy Maynard (State Street)

- Chris Funck (Chatham Financial)

- Clare Gehrhardt (DTCC)

- Dibyendu Majumdar (LCH)

- Harry McAllister (BNPP)

- Lucio Iida (Blackrock)

- Martin Sexton (London Market Systems)

- Matt Simpson (CME)

- Neal Johnston-Ward (LCH)

- Niranjana Sharma (CME)

- Paul Chellingworth (RBC)

- Prabhu Rajagopalan (DB)

- Simone Milani-Foglia (LCH)

- Sreedhar Segu (DTCC)

- Stephen White (State Street)

- Sudipto Haldar (Morgan Stanley)

- Tom Brown (OMGEO)

- Irina Yermakova (ISDA)

- Lyteck Lynhiavu (ISDA)

- Marc Gratacos (ISDA)

- Brian Lynn (Global Electronic Markets), chair

- Andy Thatai (CFTC)

- Anup Menon (Barclays Capital)

- Bruno Beccaria (Citadel)

- Bryan McRoberts (Bank of America)

- Chandra Nagavelli (Ernst and Young)

- Chris Funck (Chatham)

- Christina Yeung (GS)

- Clare Gehrhardt (DTCC)

- David Wynter (Yambina Limited)

- George Dodwell (Barclays Capital)

- George Heming (GS)

- Gordon Peery (KLGates)

- Guy Gurden (MarkitSERV)

- Harry McAllister (BNPP)

- Hector Herrera (CS)

- Henri Pegeron (MarkitSERV)

- Henrietta Johnson (Bank of America)

- Irina Leonova (CFTC)

- Jonathan Thursby (CME)

- Kate Mitchel (CFTC)

- Leon Rozin (CME)

- Ludvig Henricksson (TriOptima)

- Mark Taratko (KPMG)

- Martin Gould (DB)

- Martin Sexton (London Market Systems)

- Matt Carruth (SEC)

- Matthew Reed (SEC)

- Matt Simpson (CME)

- Miriam Steinberg (Chatham)

- Mitch Rose (CME)

- Niranjana Sharma (CME)

- Peter Salerno (DB)

- Saikat Mukherjee (Birlasoft)

- Sanjeev Shah (Jefferies)

- Sean Finnin (Societe Generale)

- Sreedhar Segu (DTCC)

- Stephen White (State Street)

- Takeo Asakura (MarkitSERV)

- Tianwei Yao (GS)

- Tony Kao (GS)

- Vinod Jain (Headstrong)

- Karel Engelen (ISDA)

- Lyteck Lynhiavu (ISDA)

- Marc Gratacos (ISDA)

- Irina Yermakova (ISDA)

- Andrew Jacobs (HandCoded Software), co-chair

- Daniel Dui (Barclays Capital and UCL), co-chair

- Mark Addison (Component Knowledge)

- Jim Brous (Metro Solutions)

- Andrew Dingwall-Smith (Message Automation)

- Ivan Djurkin (BGI)

- Marc Gratacos (ISDA)

- Lyteck Lynhiavu (ISDA)

- Christian Nentwich (Message Automation)

- Matthew Rawlings (Standard Bank)

- Irina Yermakova (ISDA)

- Harry McAllister (BNP Paribas), chair

- John Aldridge (JP Morgan Chase Bank)

- Marc Gratacos (ISDA)

- Robert Green (DTCC)

- Guy Gurden (Swapswire)

- Pierre Lamy (Goldman Sachs)

- Philippe Negri (Sungard)

- Jamie Orme (Goldman Sachs)

- Andrew Parry (JP Morgan Chase Bank)

- Marty Ross-Trevor (Bank of Tokyo-Mitsubishi)

- Marc Teichman (T-Zero)

- Jeff Valentino (Bank of America)

- Irina Yermakova (ISDA)

- Ben Lis (ICE), chair

- Kathy Andrews (Bank of America)

- Milla Bouklieva (Goldman Sachs)

- Karel Engelen (ISDA)

- Piers Evans (SwapsWire)

- Marc Gratacos (ISDA)

- Robert Green (DTCC)

- Guy Gurden (SwapsWire)

- Tony Kao (Goldman Sachs)

- Lyteck Lynhiavu (ISDA)

- Pierre Lamy (Goldman Sachs)

- Anna Lukasiak (Goldman Sachs)

- Andrew Parry (JPMorgan Chase Bank)

- Henri Pegeron (MarkitSERV)

- Mark Perry (Goldman Sachs)

- Marc Teichman (T-Zero)

- Irina Yermakova (ISDA)

- Shel Xu (Goldman Sachs)

- Simone Milani-Foglia (LCH), co-chair

- Neal Johnston-Ward (LCH), co-chair

- Marc Gratacos (ISDA)

- Richard Haslock (Logicscope)

- Andrew Jacobs (UBS)

- Kaustubh Kunte (State Street)

- Brian Lynn (GEM)

- Lyteck Lynhiavu (ISDA)

- Harry McAllister (BNP Paribas)

- Rick Schumacher (Wall Street Systems)

- Digby Strong (JP Morgan Chase)

- Stephen Turner (JP Morgan Chase)

- Mohamed Yazid (La Banque Postale)

- Irina Yermakova (ISDA)

- Christina Yeung (Goldman Sachs)

Voting Members

- Andrew Parry (JP Morgan Chase Bank), Chair

- Jasone Brasil (State Street)

- James Clark (MarkItSERV)

- Piers Evans (MarkIt)

- Robert Green (DTCC)

- Guy Gurden (MarkIt)

- Shabbir Irfani (Goldman Sachs)

- Rajan Khorana (Citadel Group)

- Robert Masri (DTCC)

- Coner Mongey

- Bin Shen (Goldman Sachs)

- Marc Teichman (T-Zero)

Non-Voting Members

- Takeo Asakura (MarkItSERV)

- Oluwasegun Bewaji (University of Essex)

- Jim Bonner (ML)

- Tom Brown (Omgeo)

- Jim Brous (Metro Solutions)

- Prashant Choudhary (Cognizant)

- Karel Engelen (ISDA)

- Philip Franz (Bank of America)

- Steve Goswell (Barclays Global)

- Marc Gratacos (ISDA)

- Vinod Jain (Headstrong)

- Lucio Iida (Barclays Global)

- Selma Laidoudi (MarkIt)

- Philip Leach (DTCC)

- Jianan Li (Citadel Group)

- Gaurav Makhija (Citadel Group)

- Mark Parris (UBS)

- Dharmender Rai

- Matthew Rawlings

- Sreedhar Segu (DTCC)

- Alicia Szybillo (DTCC)

- Sam Twum (Blue Tawny)

- Chise Yamamoto (DTCC)

- Irina Yermakova (ISDA)

- Owen King (MarkitSERV), chair

- Fatima Bentoumi (Barclays Capital)

- Hugh Brunswick (EFET Net)

- Piers Evans (Markit)

- Luis Fierro (Deutsche Bank)

- Jared Getz (Glencore)

- Marc Gratacos (ISDA)

- Anupam Gupta (JP Morgan)

- Raphael Iyageh (Goldman Sachs)

- Kiran Kodali (Citi)

- Lyteck Lynhiavu (ISDA)

- Jeffrey Magnuson (Goldman Sachs)

- Peter Stockman (DTCC)

- Digby Strong (JP Morgan)

- Irina Yermakova (ISDA)

- Brian Lynn (Global Electronic Markets), chair

- Michael Di Stefano (Integrasoft)

- Amod Dixit (Standard Chartered Bank)

- Marc Gratacos (ISDA)

- Mahmood Hanif (Bank of America)

- Pierre Lamy (Goldman Sachs)

- Philippe Negri (Sungard)

- Henrik Nilsson (TriOptima)

- Robert Stowsky (Progress)

- Vlad Efroimson (Bank of America)

- Irina Yermakova (ISDA)

- Richard Barton (Algorithmics), Chair

- Caroline Foran (HSBC)

- Anil Panchal (GlobeOp)

- Kaizad Bhathena (GlobeOp)

- Sammy Lee (GlobeOp)

- Harry McAllister (BNP Paribas)

- Jesse Nolan (UBS)

- Vivian Wu (Goldman Sachs)

- Simone Milani-Foglia (LCH Clearnet)

- Nicole Jolliffe (SWIFT)

- Evelyne Piron (SWIFT)

- Chip Miller (JPMorgan)

- John Straley (DTCC)

- Joe Novellino (DB)

- Lucio Iida (Blackrock)

- Tom Brown (Omgeo)

- Benjamin Riley (Deloitte and Touche)

- Marc Gratacos (ISDA)

- Irina Yermakova (ISDA)

- Lyteck Lynhiavu (ISDA)

The Financial Products Markup Language (FpML) is the industry standard enabling e-business activities in the field of financial derivatives and structured products. The development of the standard, controlled by ISDA (the International Swaps and Derivatives Association), will ultimately allow the electronic integration of a range of services, from electronic trading and confirmations to portfolio specification for risk analysis. All types of over-the-counter (OTC) derivatives will, over time, be incorporated into the standard.

FpML is an application of XML, an internet standard language for describing data shared between computer applications.

The FpML Reporting Working Group has defined two new views, "Transparency" and "Recordkeeping", to support parties and execution facilities reporting trading activity into Swaps Data Repositories (SDRs), as required by the Commodities Futures Trading Commission's 17 CFR 43 and 45, and similar requirements from the Securities and Exchange Commission in 17 CFR 240. The FpML Standards Committee invites comments on the proposed materials including schemas, examples, and documentation.

In WD#2, a number of new products have been added to Transparency view. The changes versus Confirmation view have been modeled on other products in WD#1, but the product representations have not yet been reviewed in detail in the working group. The FpML Reporting Working Group invites feedback on the detailed contents in Transparency view of any product.

The FpML Business Process Working Group has adjusted the multiplicity of the correlation IDs and is seeking feedback on this change. In particular, is there a need for multiple correlation IDs if the correlation ID on original requests is made optional?

Comments on this document should be sent by filling in the form at the following link: http://www.fpml.org/issues.

- Business Process:

- Added the ability to specify more than one Notional on a single Allocation: Within 'Allocation' complex type, the cardinality of the element 'allocatedNotional' has been changed to 1..2.

- Rationale: Needed for proper representation of certain multi-leg or multi-notional products.

- Added the ability to specify a relevant party, such as Clearing Broker, at the Allocation level: Within, AllocationContent.model group added a new optional element 'relatedParty' of RelatedParty type.

- Rationale: To allow for the ability to specify any relevant parties at the allocation level. This requires for any clearing flows in which the determination of certain entities, such as Clearing Broker, are handled outside of the CCP and are submitted directly by the client.

- Added the ability to specify more than one Notional on a single Allocation: Within 'Allocation' complex type, the cardinality of the element 'allocatedNotional' has been changed to 1..2.

View PDF for details on schema changes

View PDF for details on validation rules changes

View SCHEME DEFINITIONS for details on coding schemes changes

- Reporting and Business Process:

- Trade and Termination Events

- Added the optional "originatingEvent" element to generic messages when the event is a new Trade. This element allows the sender to provide additional explanation as to why the new trade was created. Also added a corresponding coding scheme.

- Added the optional "terminatingEvent" element to generic messages when the event is a Termination. This element allows the sender to provide additional explanation as to why the new trade was terminated. Also added a corresponding coding scheme.

- Added the ability to specify more than one Notional on a single Allocation: Within 'Allocation' complex type, the cardinality of the element 'allocatedNotional' has been changed to 1..2.

- Rationale: Needed for proper representation of certain multi-leg or multi-notional products.

- Added the ability to specify a relevant party, such as Clearing Broker, at the Allocation level: Within, AllocationContent.model group added a new optional element 'relatedParty' of RelatedParty type.

- Rationale: To allow for the ability to specify any relevant parties at the allocation level. This requires for any clearing flows in which the determination of certain entities, such as Clearing Broker, are handled outside of the CCP and are submitted directly by the client.

- Consent Negotiation

- Added the optional "requestedAction" element to indicate why consent is being sought, and a corresponding coding scheme.

- Added documentation to describe how the consent negotiation messages can be used to request consent for clearing a trade.

- Maturity Notification

- Added a new message that can report on trades that have matured. This can be used for options that have expired or any trade that has passed its final event and can be removed from the active portfolio.

- Message Framework:

- Correlation IDs and sequence numbers have been made optional for initial requests and notifications.

- Allowed exception messages to include the original message as unvalidated XML.

- Allowed acknowledgement messages to include the original message as unvalidated XML.

- Added enhancements to report trade amalgamation (netting, compression).

- Added enhancements to handle portfolio requests (portfolio-type business processes).

- Business Process:

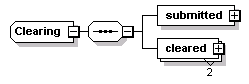

- Added a "Clearing" Event as an available event type in clearing messages.

- Allowed tradeReferenceInformation (IDs and trade information) to be reported in place of full trade/event details in a number of messages

- Enhanced the clearing status message to allow information about which parties are affecting status (e.g. pending approval to clear)

- Added the ability to record valuation information (quotes) for many event messages

- Added the "TradeReferenceInformationUpdate" process to allow identifying information such as trade IDs to be updated for existing trades.

- Provide more examples of consent messages for clearing, with additional details.

- Allowed acknowledgment messages for most event requests to contain summary information such as trade IDs, to allow acknowledgers to supply additional identifying information about trades.

- Updated partyTradeInformation to include all fields from recordkeeping view (as optional).

- Within ClearingStatus->ClearingStatusItem complex type, added an optional 'reason' element within to explain the reported clearing status value to message consumers.

- Reverted the maximum cardinality of onBehalfOf to 0..1 in Confirmation view. Rationale: The Business Process Working Group formally voted in favor of reverting the cardinality of onBehalfOf in Confirmation view to 0..1 since the use case for more than 1 onBehalfOf has not been established.

- Within RequestEventStatus->EventIdentifier and EventStatusItem->EventIdentifier complex types, the Business Process Working Group decided to deprecate the sequence number to avoid misuse as sequence number does not make sense in this context.

- Trade and Termination Events

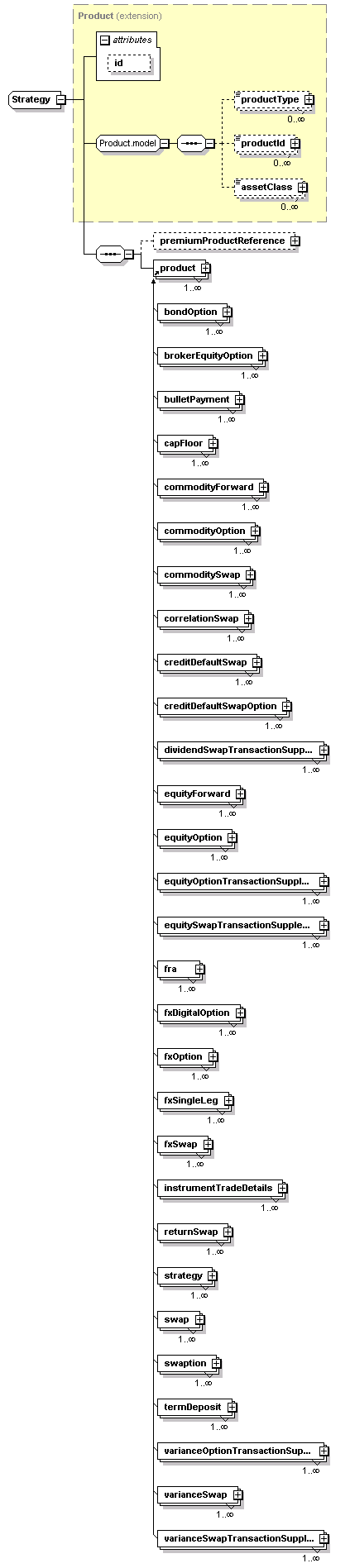

The scope of FpML 5.2 includes broadened BusinessProcess/Messaging coverage and additional product support, specifically:

The various Working Groups have developed FpML 5.2 within the FpML Architecture 3.0 Specification defined by the Architecture Working Group. This document defines that standards and principles on which the FpML grammatical definitions are based.

The FpML Architecture 3.0 builds upon the earlier FpML Architecture specifications and the conventions of FpML 1.02b before that. The refinement of the FpML architecture is an evolutionary process bought about by changes in the XML technology upon which it is based and the requirements of the standard as its scope expands.

The FpML Messaging Task Force group was formed to define a new messaging framework that insures consistent processes across trades and post-trade events, observable completion, consistent message correlation, consistent error reporting, consistent correction and retraction.

Most of the FpML 5 business processes are “generic” processes that can apply to new trades and/or any post-trade events. This means that the message name indicates the business process (e.g. confirmation, execution notification, etc.) but not the type of event (e.g. trade, amendment, etc.). The payload of the message indicates the type of the event.

The business processes currently supported include:

1.7.2.1 Generic processes:

1.7.2.1.1 Post-trade

- Execution notification (for platforms to report order fills)

- Execution advice (to report executions and settlement info to service providers)

- Allocation (expanded for version 5)

- Confirmation

- Consent negotiation

- Clearing (new for version 5)

- Status reporting

1.7.2.2 Generic (Multi-Event) Flows

All the processes described in this section are applied to the following events:

- trade

- novation

- increase

- termination

- amendment

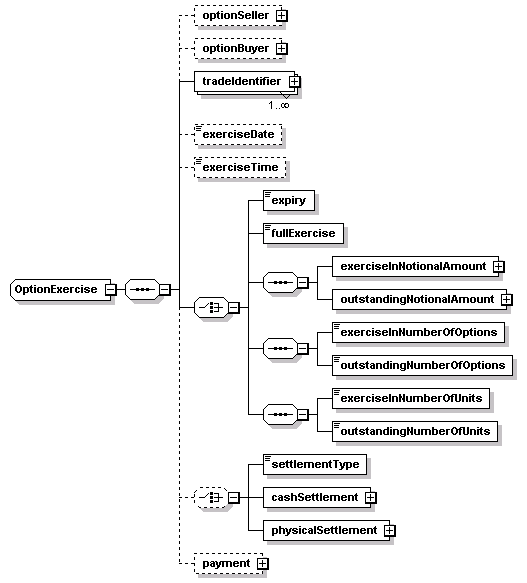

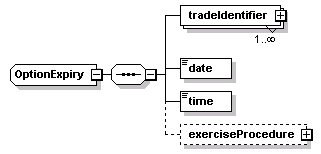

- option exercise / option expiry

- deClear

To support these business processes, a number of messages have been defined. Please see the "Business Process Architecture" section for more information.

The Validation Working Group provides semantic, or business-level validation rules for FpML 5.2. These validation rules, which are aimed at normalizing the use of elements within FpML, are issued as part of the FpML Specification in the validation section of this document.

The validation working group publishes with its releases:

- A set of rules described in English

- Positive and negative test case documents for each rule

- Non-normative reference implementations

The current specification includes a set of rules for Interest Rate Derivatives, Equity Derivatives, Credit Derivatives, Loans, FX, and for shared components. The rules for the different asset classes will be further enhanced in future versions.

In FpML 5.2 Reccomendation #2 the following Interest Rate Derivative products are covered:

- Single and Cross-Currency Interest Rate Swap

- Forward Rate Agreement

- Interest Rate Cap

- Interest Rate Floor

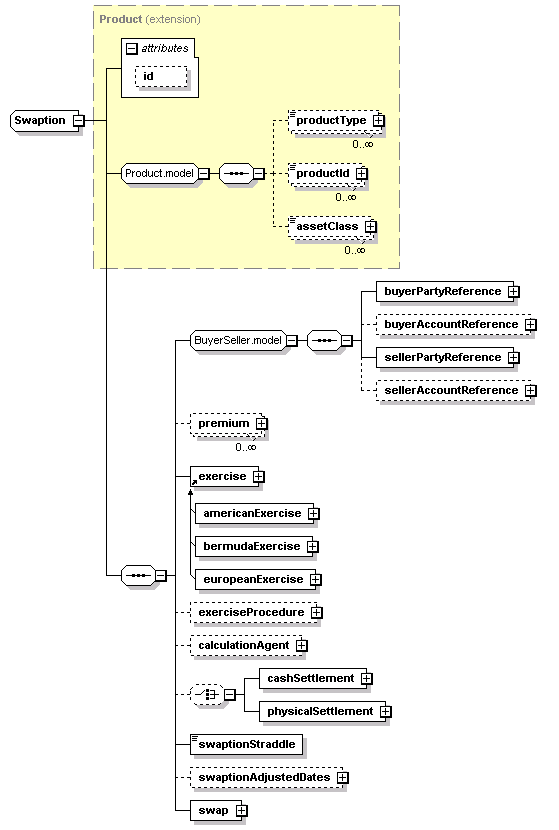

- Interest Rate Swaption (European, Bermuda and American Styles; Cash and Physical Settlement)

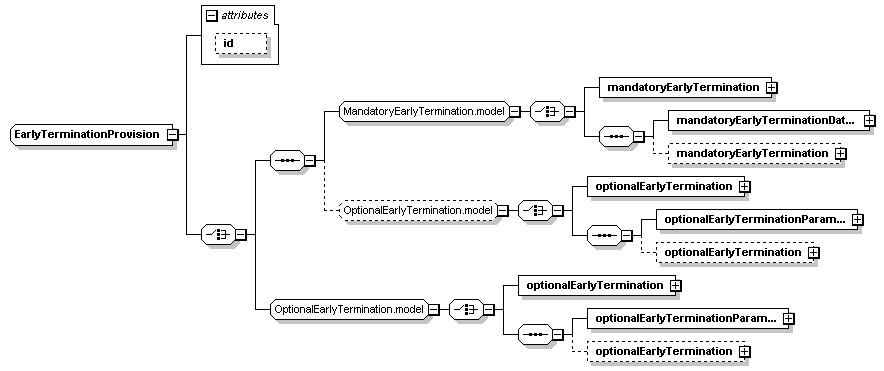

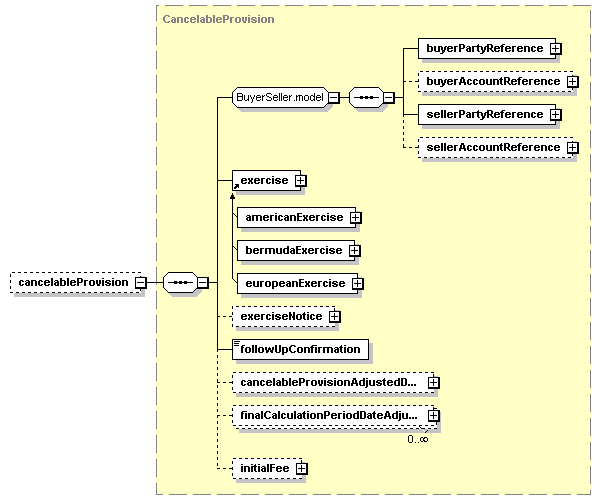

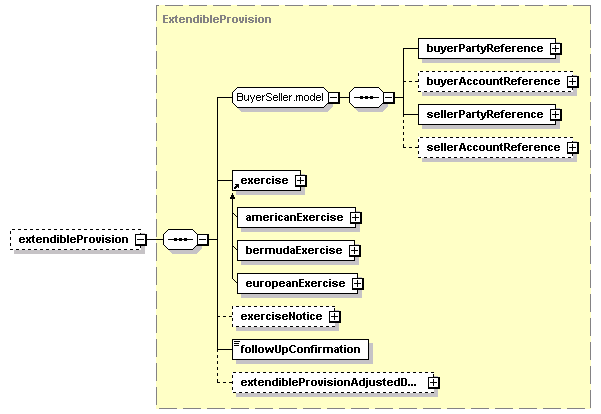

- Extendible and Cancelable Interest Rate Swap Provisions

- Mandatory and Optional Early Termination Provisions for Interest Rate Swaps

- FX Resetable Cross-Currency Swap

In FpML 5.2 Reccomendation #2 the following Credit Derivative products are covered:

- Credit Default Swap

- Standard Coupon Credit Default Swap

- Credit Default Swap Index

- Tranche on Credit Default Swap Index

- Credit Default Swap Basket

- Credit Default Swap on a Mortgage

- Credit Default Swap on a Loan

- Option on Credit Default Swap

- Credit Event Notice

The Scope of FpML 5.2 Reccomendation #2 includes redesigned FX product model developed by the Modeling Task Force (MTF) and FX Working Group to make it more consistent with other FpML product representations and to facilitate its further development. As a result of this work many of an original 4.x model’s issues were addressed:

- A number of sets of reusable components that facilitates product development were defined, so that the existing and future FX products will leverage these building blocks to ensure the FX model is coherent and easy to maintain, as per FpML best practices

- Extended the existing coverage to include Dual Currency Deposits.

- Rationalized the models' constraints:

- Made use of grammar to bring related data together.

- Made better use of XML schema to simplify the validation rules.

In FpML 5.2 Reccomendation #2 the following FX products are covered:

- Basic FX Products

- FX Spot and FX Forward (including non-deliverable settlements, or NDFs)

- FX Swap

- Simple FX Option Products (including, features, cash and physical settlement)

- FX options

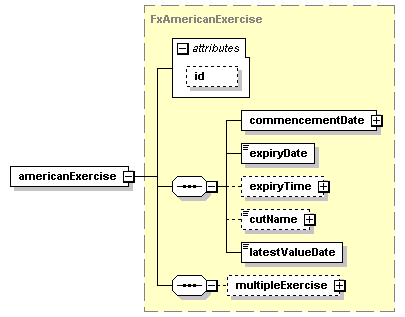

- European and American

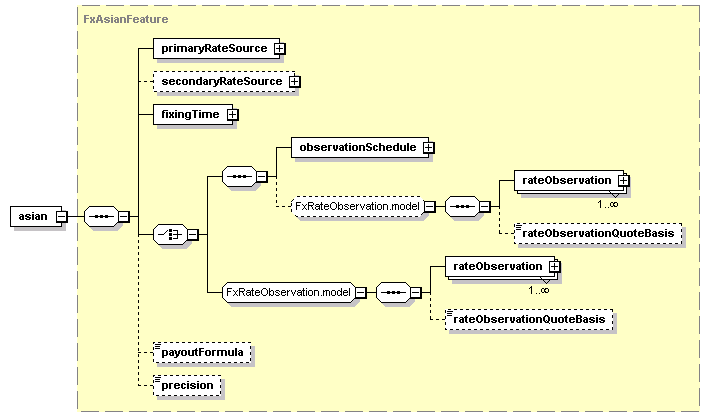

- Averaging

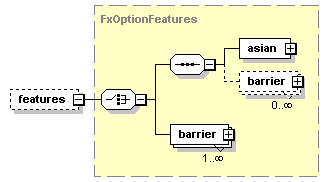

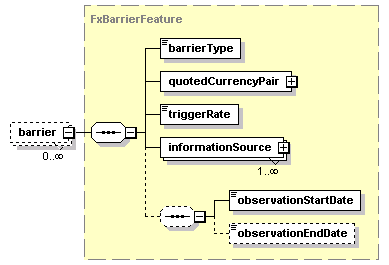

- Barriers

- Digital Options

- FX options

- Option Strategies (multiple simple options)

In addition, support for the following money market instrument is also provided:

- Term Deposits (including features)

- Money Market Deposits

- Dual Currency

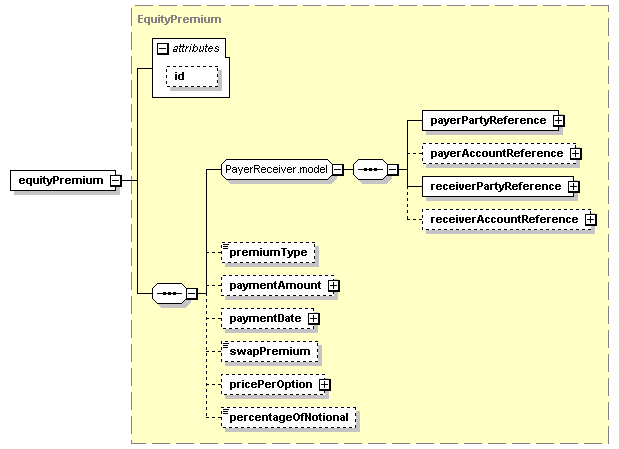

The EQD Products Working Group has extended the FpML standard to cover the following Equity Derivative products

- Broker Equity Options;

- Long Form Equity Forwards;

- Long Form Equity Options;

- Short Form Equity Options represented as Transaction Supplements under ISDA Master Confirmation Agreements.

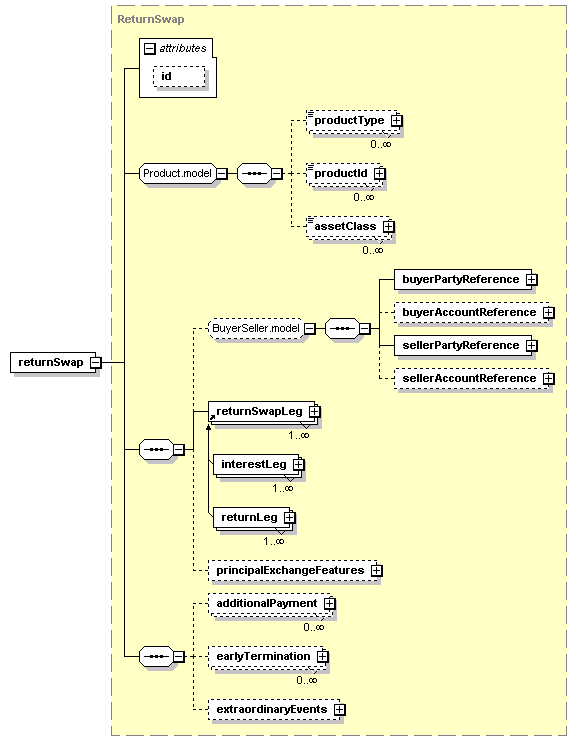

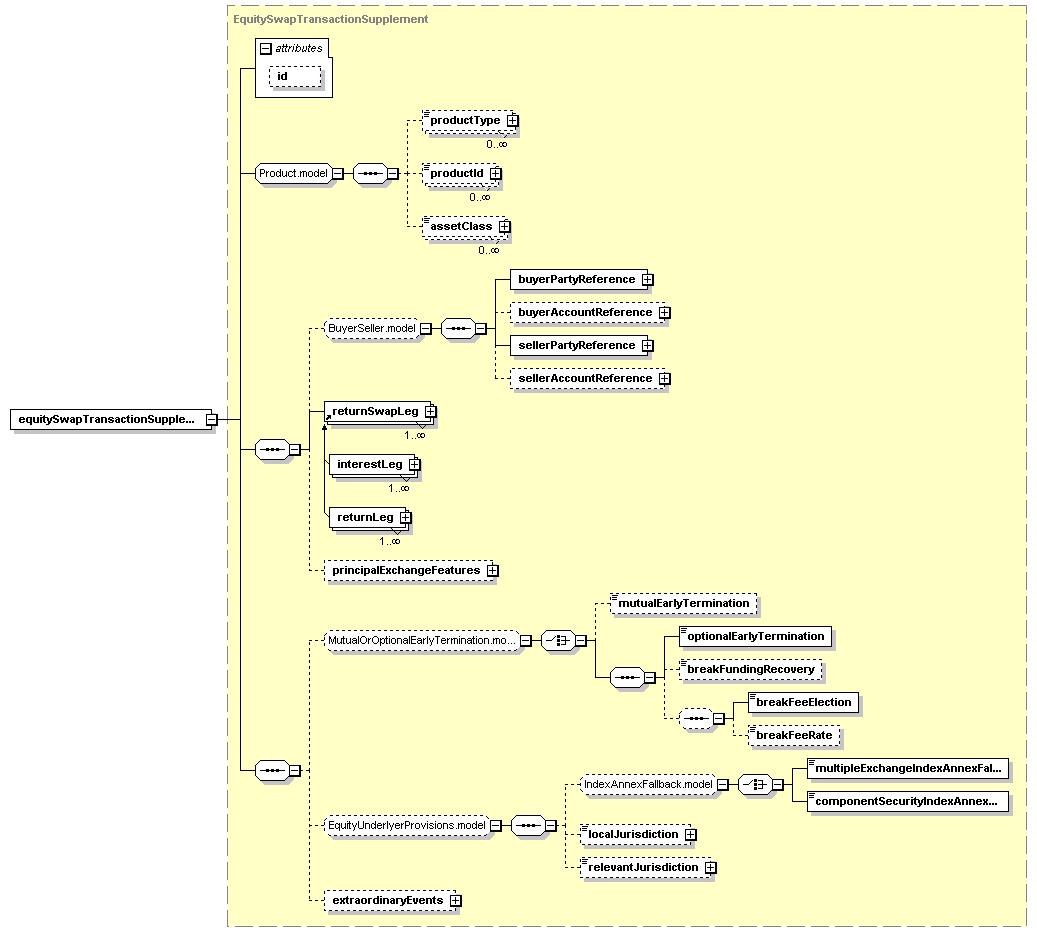

FpML provides generic Return Swaps support including "long form" Equity Swap representations, as well as Total Return Swaps. A separate product element called equitySwapTransactionSupplement supports "short form" Equity Swap Transaction Supplement.

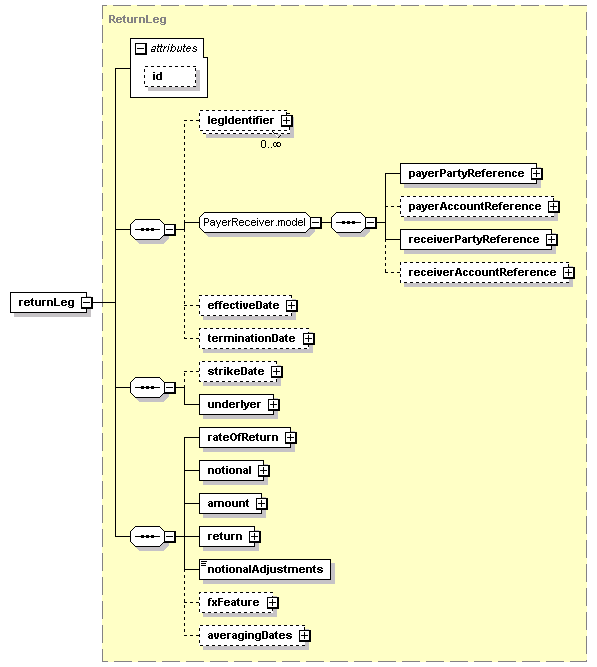

Return-type Swaps have 1-to-many Legs, all of which must be derived from the ReturnSwapLeg type. Instances of Legs are returnLeg, interestLeg. Other Leg types may be derived from ReturnSwapLeg at will, to allow for private extensions to support whatever type of Generic Return Swap is desired.

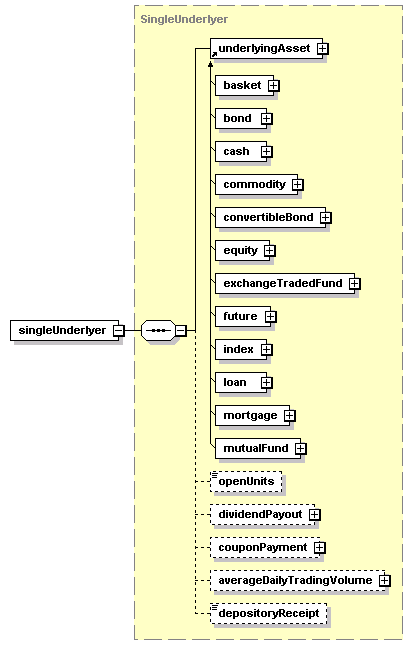

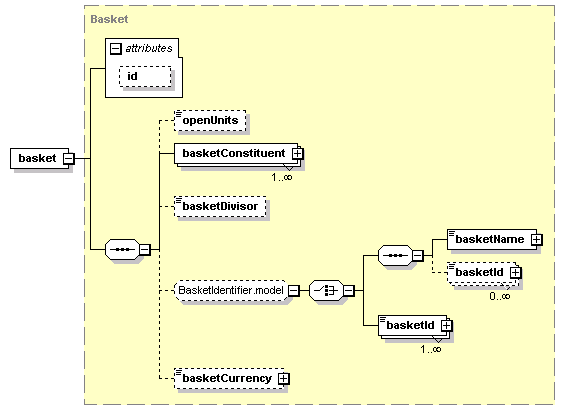

The scope of this FpML representation for return swaps is to capture the following types of swaps that have equity-related underlyers:

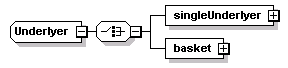

- Single stock swaps as well as basket swaps (i.e. swaps with multiple underlyers);

- Swaps that have a different types of underlying assets (equity, index, mutual funds, exchange-traded funds, convertible bond, futures), or a combination of these;

- 2-legged swaps with a combination of an equity leg and a funding leg, as well as swaps that either have only one leg (e.g. fully funded or zero-strike swap) or multiple equity legs (e.g. outperformance swaps);

- Total Return Swaps, a type of swap in which one party (total return payer) transfers the total economic performance of a reference obligation to the other party (total return receiver).

- Swaps that have specific adjustment conditions, such as execution swaps or portfolio rebalancing swaps;

- Swaps that involve the exchange of principal cashflows;

- Swaps that have inital and final stubs;

- Swaps which can be represented as Transaction Supplements under ISDA Master Agreements;

Extraordinary Events terms have been incorporated, to take into consideration the release of the 2002 ISDA Definitions for Equity Derivatives.

Trigger swaps, in which equity risk morphs into a fixed income risk once a certain market level is reached, may be supported in a subsequent release.

The Equity Derivative Working Group extended FpML to cover:

- Correlation Swaps

The Equity Derivative Working Group extended FpML to cover:

- Variance Swaps, a type of volatility swap where the payout is linear to variance rather than volatility, therefore the payout will rise at a higher rate than volatility;

- Short Form Variance Options represented also as Transaction Supplements under ISDA Master Confirmation Agreements.

The Equity Derivative Working Group extended FpML to cover:

- Dividend Swap Transaction Supplement

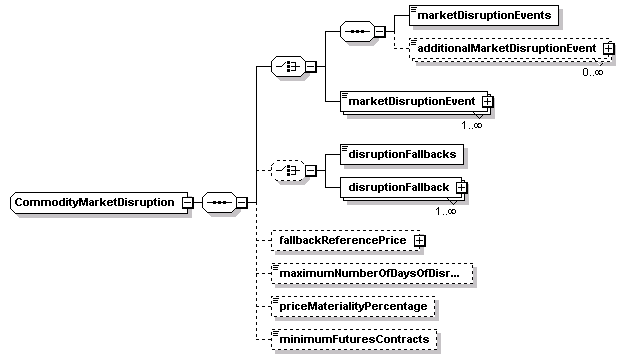

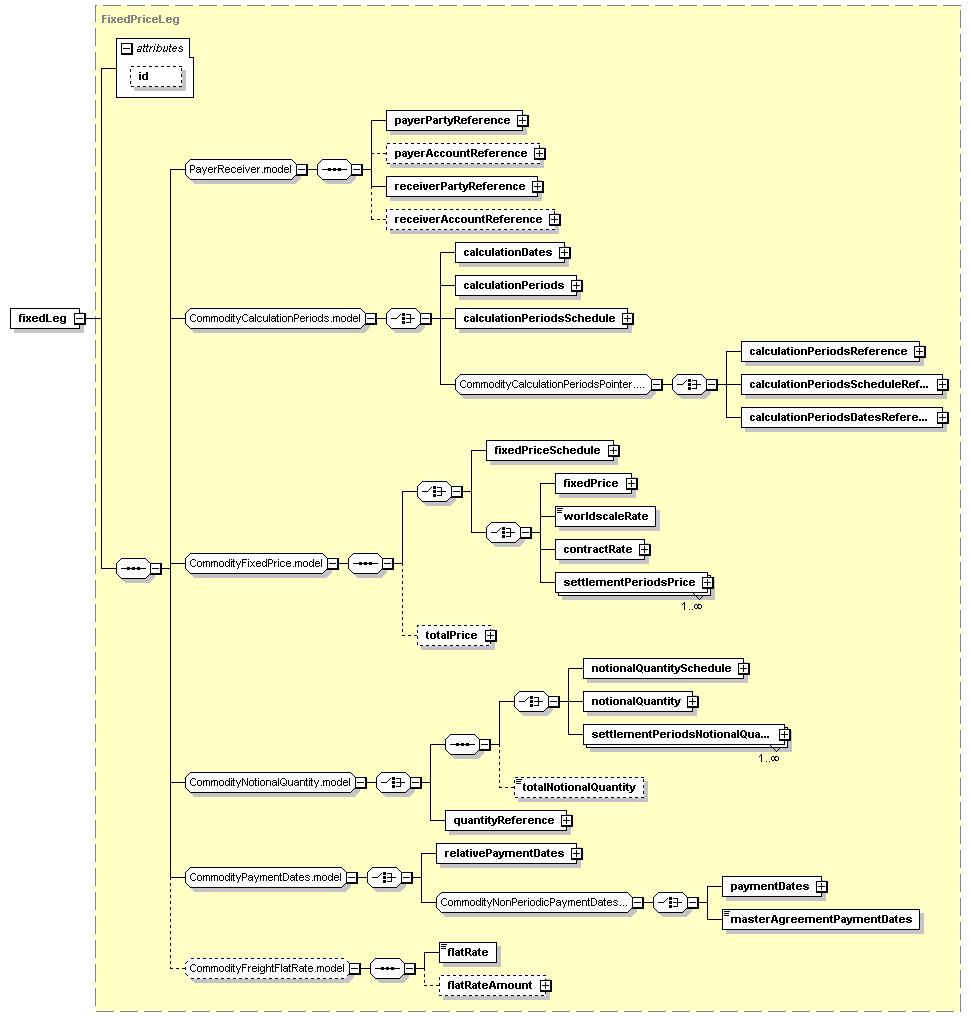

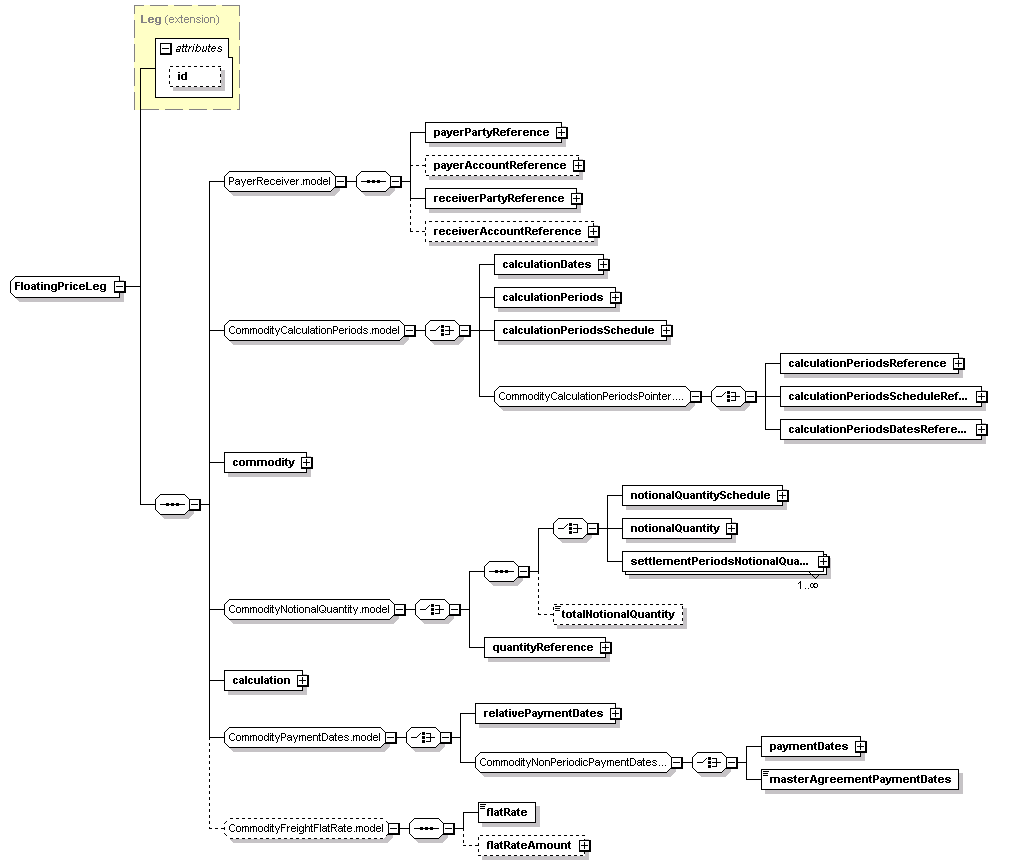

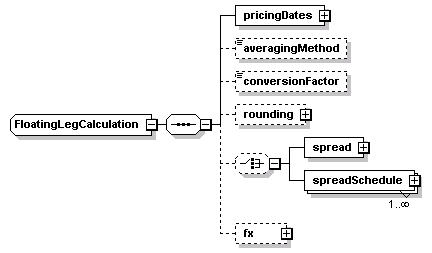

The Commodities Working Group will extend the FpML standard to include trade types and products for the OTC commodities markets, following the structure and coverage of the 2005 ISDA Commodity Definitions. The following are included in version 5-2:

- Support for financially settled swaps, options and spreads

- Support for physically-settled swaps/forwards, options

- Natural Gas, Oil, Electricity, Coal as the underlying Commodity product

Business Process is including Confirmations, Valuations, Reporting

Producers of FpML documents intended for interchange with other parties must encode such documents using either UTF-8 or UTF-16. Consumers of FpML documents must be able to process documents encoded using UTF-8, as well as documents encoded using UTF-16. For more information, see

Unrestricted FpML elements may use any valid XML characters. For more information, see

http://www.w3.org/TR/REC-xml#charsets

Certain elements and attributes (such as scheme URIs) are defined with more restrictive types, such as xsd:normalizedString, xsd:token, or xsd:anyURI. For these types, please see the relevant data type definition in the XML Schema datatypes specification:

capFloor

capFloor