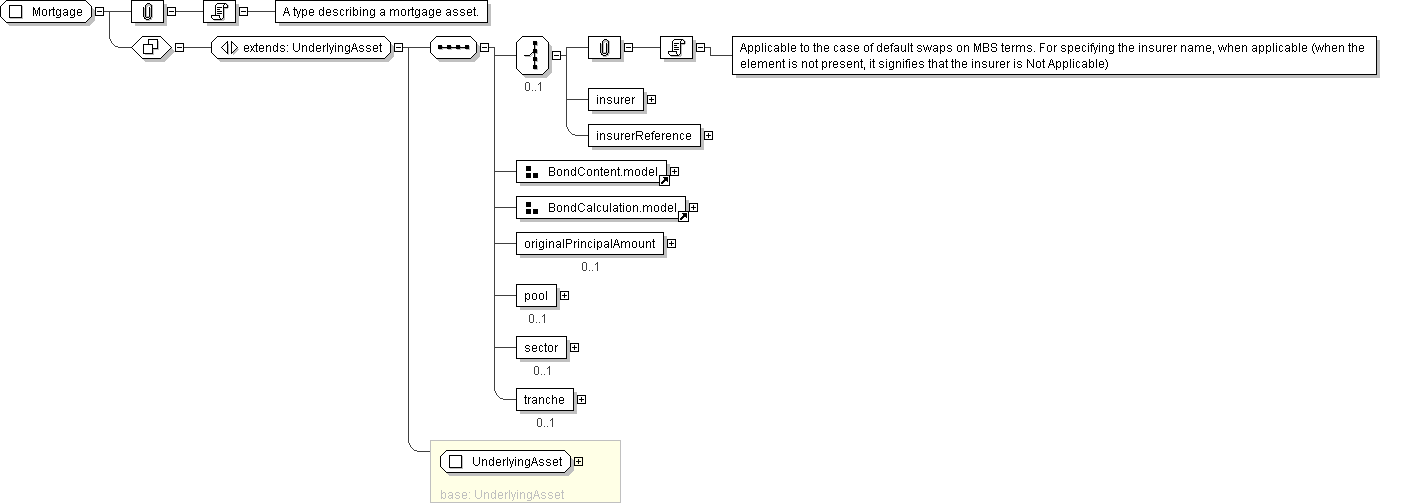

Diagram

| Super-types: | Asset < IdentifiedAsset (by extension) < UnderlyingAsset (by extension) < Mortgage (by extension) |

|---|---|

| Sub-types: | None |

| Name | Mortgage |

|---|---|

| Used by (from the same schema document) | Element mortgage |

| Abstract | no |

| Documentation | A type describing a mortgage asset. |

'Identification of the underlying asset, using public and/or private identifiers.'

'Identification of the exchange on which this asset is transacted for the purposes of calculating a contractural payoff. The term \"Exchange\" is assumed to have the meaning as defined in the ISDA 2002 Equity Derivatives Definitions.'

'Identification of the clearance system associated with the transaction exchange.'

'An optional reference to a full FpML product that defines the simple product in greater detail. In case of inconsistency between the terms of the simple product and those of the detailed definition, the values in the simple product override those in the detailed definition.'

'Applicable to the case of default swaps on MBS terms. For specifying the insurer name, when applicable (when the element is not present, it signifies that the insurer is Not Applicable)'

'Specifies the issuer name of a fixed income security or convertible bond. This name can either be explicitly stated, or specified as an href into another element of the document, such as the obligor'

'Specifies if the bond has a variable coupon, step-up/down coupon or a zero-coupon.'

'Specifies the coupon rate (expressed in percentage) of a fixed income security or convertible bond.'

'The date when the principal amount of a security becomes due and payable.'

'Specifies the frequency at which the bond pays, e.g. 6M.'

'The initial issued amount of the mortgage obligation.'

'The mortgage obligation tranche that is subject to the derivative transaction.'